Residential Rental Properties: The Fundamentals

How residential rentals work and how to make money with them.

Shoutout to Hannah for the prompt on this one! Specifically, this post is going to be focused on residential rental properties, which are the type that most of us are probably somewhat familiar with.

What are Residential Rental Properties?

Residential rental properties are homes that are purchased by an investor and inhabited by tenants on the terms of a lease or another rental agreement. Property owners who rent out their property are known as landlords, while those who inhabit the properties are referred to as tenants.

Residential property is zoned specifically for living or dwelling for individuals or households, ranging from single-unit family dwellings to large, multi-unit apartment buildings. It also includes things like townhouses, duplexes, and condominiums.

Law requires that a property has to derive 80% of its income from residential purposes to qualify as residential for tax purposes. The tenants in residential rental agreements will be people who need a personal place to live, whereas with commercial rentals, the tenant would be some kind of profit-seeking corporate entity. There are also hotels, motels, and rental apps (like Airbnb) which can classify agreements as short-term rentals.

The Benefits

Residential rental properties can offer monthly cash flows, long-term appreciation, leverage using borrowed funds, and tax advantages on the income produced by the rental agreement. In the case that an investor indirectly places money in a real estate investment trust (REIT), they would not be conferred any tax benefits offered by the security, so owning outright has an edge.

In short, property owners stand to benefit from 1) steady cash flows, 2) property appreciation, and 3) tax benefits.

The Risks

Landlords are at risk of vacant units, difficult tenants, and any unplanned upkeep or maintenance that comes with owning a rental property, as well as potential fluctuations in the market value of of the rental itself. Property investments are also not very liquid, meaning that mismanagement and market conditions can backfire on the landlord and leave them holding the bag on a bad investment. Tax codes are also subject to change, meaning that landlords might be subject to tax increases or changes in tax benefits based on governing bodies.

Tax Treatment of Rental Properties

Residential rental property uses the 27.5-year modified accelerated cost recovery system (MACRS) schedule for depreciation. Rental income is treated as passive income, so there are rules around how losses are treated based on participation of the owner. The IRS publication 527 Residential Rental Property has an overview of the tax rules for residential rentals and is updated when rules or provisions change.

The Different Avenues You Can Take

Single-family homes: These are detached houses that are designed for one family. They often attract long-term tenants and can boast high appreciation in value, but managing a single unit means that vacancy will result in a full loss of rental income for that specific period.

Multi-family properties: Buildings containing multiple separate housing units, such as duplexes, triplexes, fourplexes, and apartment buildings. These can offer consistent cash flow due to having multiple tenants, and the cost per unit can be lower than single-family homes. The challenge with these is that they often require more intensive upkeep and management.

Condos & Townhouses: Individual units within a larger complex, often with shared walls and common areas. Ownership typically comes with a Homeowners Association (HOA) that collects monthly fees to cover the maintenance of shared amenities and exterior.

Short-Term Rentals: Properties rented out for short periods, often through platforms like Airbnb/Vrbo, that cater to tourists and business travelers. These have the potential to generate higher income, but also have more frequent tenant turnover, intensive management, and can be subject to specific regulations.

Becoming a Landlord: Walkthrough

I’m going to lead with the disclaimer that if you’re just looking for a way to grow your wealth without doing any work, this is probably not the ideal avenue to take. If you want to grow wealth without putting effort in, your best bet is likely to invest in broad-market index funds or things like HYSAs.

That being said, housing is always in demand, and relying on your own efforts rather than fully placing your wealth in externally managed vehicles is a wise move. If you’re willing to be a responsible landlord, this can be a great route to take.

Example of How Rental Properties Build Wealth

*Disclaimer: I am using relatively simple examples here that rely on assumptions.

Let’s say you want to buy a rental property for $200k total, and you’re able to put 20% ($40k) down in order to not have to purchase Private Mortgage Insurance (PMI). This means that you’ll have to work with a lender to secure a mortgage for the remainder needed to purchase the home. For this specific example, you’ll need a loan of $160k, and we’ll assume that the loan is a 30-year fixed-rate loan with an interest rate of 6.6% (this is about where the current loan market is at).

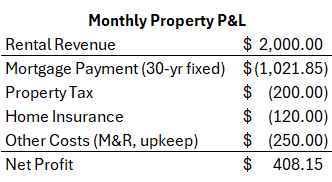

The mortgage alone will cost you $1,021.85 per month before incurring any additional expenses like property taxes, insurance, maintenance & repairs, etc. We then have to add in property taxes of $200 per month (there are so many regulations and laws around these by geography, but let’s just assume 1.2% annual of total property value). Let’s also assume that you have to insure the home for $120 per month, and that you have no HOA and will be responsible for maintaining the property at roughly $250 per month (there’s a rule of thumb stating that you should expect to spend 1% of the property value each year on upkeep). After adding together all of these expense, you can expect expenditures of roughly $1,591.85 per month to service the property. There are also one-time costs upon closing on a house which include closing costs, as well as any updates the buyer has to pay for (paint, furniture, appliances, etc.)

Next, we have to ask the obvious question: how much should you charge for rent? You should be able to use readily available information on nearby properties to develop comparisons, but the rule of thumb is to charge 1% of the property’s value for monthly rent, which would come out to $2,000 per month in this specific example. Given this information, we can expect to make a profit of $408.15 per month ($4,897.80 per year) if everything goes smoothly. Not life changing money by any stretch, but we do come out ahead here. The monthly P&L would look something like the below:

The big opportunity lies in the property’s ability to appreciate, as well as the fact that your tenants are building equity for you. The biggest threats, in my eyes, are occupancy and the potential for irresponsible tenants. You’re on the hook for a pretty substantial monthly bill if nobody is renting the property from you, and holding tenants accountable for damages or late payments can be a very painful process.

If your property appreciates by 5% a year (the average for US homes in the last decade), the total value in five years for this example will be worth around $255,256; using an amortization table, I’ve calculated that the tenants will have paid for about $10,051.29 of equity from the loan (yes, shocking how much of the early loan payments go to interest), so in total, you will have about $105,307.29 of equity built up in the property ($40k down payment + $10,051.29 of equity from paying the loan + $55,256 of property value appreciation).

This doesn’t mention that you’ll also be able to raise the price of rent in accordance with property value, though you’ll also pay more in expenses due to a higher valuation and inflation. The adjusted P&L might look something like this after accounting for those changes after five years:

Not to mention, you can also refinance loans if and when interest rates start to come down. A refinance is when you agree to replace the existing terms of a credit agreement with a new one; essentially, you take a new loan out to pay off your existing one, usually to get better interest rates. If interest rates drop to, say, 4%, and the loan is five years in, you’ll have around $149,949 remaining on your initial loan. You can negotiate a new loan for that amount at 4%, which would drive your monthly mortgage down to around $791.49 and save you around $68k over the lifetime of the entire loan! You’d definitely have to pay some up front costs to service the new loan, but it wouldn’t take long to come out ahead by refinancing.

Let’s build out a new P&L with the refinance detail:

So, if you hold this property for 5 years and things go smoothly, you could have $105,307.29 of equity built up and be generating monthly net profit of over $1,036.01, not to mention receiving tax benefits from it! Of course, you’d have to have very reliable tenants and steady market conditions to pull this off, so there are never any guarantees. It’s also possible that a major incident takes place, such as the furnace giving out, which would be a massive and unexpected expense for the landlord of the property.

My Takeaway

Property is a sound investment vehicle, but like any other investment, there are some factors that are out of your control. It’s one of the best ways to gain access to leverage (using loans to increase investment returns) for someone who doesn’t work in finance & banking, and it has historically provided landowners with property appreciation and stable cash flows.

If you want to win with residential real estate, you need to keep a high occupancy rate and make sure that you are properly vetting your tenants. Find areas that are economically stable, have low rates of natural disaster, and have strong labor markets and steady/growing populations. Make sure that the places you buy are inspected and don’t come with any major foreseeable risks like infestation or massive repairs.

Early on, unless you hire a property manager, I would not consider this to be passive income. You’re going to have to be actively involved with the upkeep of the property and dealing with tenant needs as they arise, and some seasons will be busier than others. If you go the slumlord route, expect to have an abundance of problems that go way beyond making money.

This post is pretty general, but I hope that it’s helpful! Feel free to reach out with any specific questions if you’d like more specifics on certain landlord topics (regulation, taxes, tenant challenges, etc).

To appreciation & cash flows,

Jared